Construction Cost Visibility: Why Financial Tracking Breaks as Projects Scale?

What Really Changes on the Ground?

There can be many reasons that a construction project manager can come up with for justifying financial mistakes, but most of the time the problem is inaccurate bookkeeping, and this happens because of a lack of visibility and accurate reflection of how projects unfold in real time. Since it is easier to choose accounting tool, many contractors end up doing that. It indeed helps in invoicing, salaries, vendor payments, and tax efficiencies. But it suits small businesses with limited projects. Although, a construction business does not remain limited to merely one to two projects. It expands, teams multiply, subcontractors increase, approval processes grow layered, and suddenly, you appear far away from what is exactly happening on the site. That gap is where profit erodes quietly. In this article, we will discuss Construction cost visibility and Why Financial Tracking Breaks as Projects Scale?

How Transaction-Based Financial Tracking Works in Construction?

Transaction-Based Financial Tracking is designed primarily to organize financial information.

Its purpose is clear:

- Record revenue and expenses

- Maintain ledgers

- Handle payroll and statutory deductions

- Generate financial statements

- Ensure tax compliance

A Transaction-Based Financial Tracking works like wonders for businesses that requires structured bookkeeping. Once a transaction is made, it can be recorded and categorized accurately. In the same way, if material is purchased, the invoice is made in this accounting software. If a subcontractor is being paid, that payment log is being recorded in the accounting software. If a payroll cycle runs, the entries are generated. This system helps in providing visibility and clarity that has been occurring financially. However, it does not give real-time visibility and cannot affect financial decisions of a construction company. It is only useful after the events have taken place.

What Changes When Financial Control Is Linked to Execution?

When Financial Control Is Linked to Execution you can watch real-time activities that are happening at a construction site and get better construction cost visibility. It is built around the idea that financial performance in construction directly depends on everyday activity on the site. Instead of focusing on ledger entries, ERP platforms direct a construction project to have a connected planning, execution, and accounting in a single framework.

A Financial Control Is Linked to Execution system typically integrates:

- Project budgeting and BOQ

- Purchase approvals and supplier management

- On-site progress recording

- Subcontractor billing and retention tracking

- Labor and material consumption data

- Project-level financial reporting

With the help of this system, the focus shifts from documentation of expenses to the supervision of cost management.

Can Excel and Manual Tracking Keep Up with Growing Construction Projects?

Many businesses start their record-keeping from spreadsheets because they’re easily accessible and easy to use. It also is inexpensive. By using spreadsheets, construction firms make budget in one file, along with purchase details in another, and subcontractor payments in third, and so on. Initially, this process seems just fine. The limitations occur when construction projects scale. There might be arithmetic accuracy in the spreadsheets, but a construction project needs real-time monitoring. If we take a common example:

A construction site places an order of reinforcement steel and the supplier delivers it to the site. The invoice reaches accounts. Later, someone updates the cost sheet to adjust totals against the budget. The number will come out accurate, but the review happens after this whole process has been done, when decisions have been made and the payout has taken place. This is spreadsheet document history. They do not actively monitor exposures as it forms.

As workload increases, so does spreadsheet volume:

- Separate sheets for budget planning

- Purchase registers maintained manually

- Subcontract bills tracked independently

- Labor costs reconciled in another file

These files are modified at different intervals by different team members. Most of these versions regulate across email and errors are common to happen. Repetitive cross-checking should be in your routine if you are using spreadsheets. The consolidated data turns into a recurring effort rather than a strategic review. And the major issue is timing. Costs overrun only show up during reconciliation, not when it is happening in present. By the time of reconciliation, materials have been installed and payments have already been made.

How Profit Slips Without Warning?

Cost Exposure Exists Before It Is Logged

In actuality, the moment a site is chosen, financial commitment begins. Materials are ordered. Workers are enlisted. The scope of a subcontract grows.

However, formal recognition typically doesn’t start until invoices are recorded in the books. On-site, the cost had already begun to take shape by then. The accounts may be accurate.

The visibility is late. That gap is where financial danger subtly accumulates.

Subcontract Scope Expands Gradually

Subcontract packages rarely change through one major revision. It changes every day along with minor adjustments like extra reinforcement being added on instruction, any random small finishing items being included informally, and productivity gaps that increase the work hours. As individuals, they seem manageable problems, but as the project progresses, it collectively alters the financial structure of the contract. When the cost is not being reflected alongside execution, marginal adjustments happen gradually and silently.

Material Overuse Becomes Visible After the Fact

The problem in material management often occurs from unplanned wastage, on-site corrections, measurement discrepancies, and minor design adjustments. If this consumption of material is not reviewed against planned quantities in real time, the differences appear only after the work, and the loss is being done. At that point, most of the material has been overused and remedial options are limited.

Financial Risk Advances Faster Than Reporting Cycles

Execution takes place every day. Financial review often moves monthly. When reporting intervals trail operational pace, exposure builds before leadership sees it. This gap between activity and awareness is the core dynamic of margin fade.

Progress Approval Without Cost Reassessment

When in-need quantities are approved on-site for operational reasons, but those approvals may trigger an immediate revision on what was planned, it is necessary that physical progress and financial implication go hand in hand. When they do not, margin assumptions remain outdated.

Retention Managed Through Manual Adjustments

Retention amounts often need to be recalculated across billing cycles. When this is done manually and reviewed outside the broader cost forecast, inconsistencies can creep in from one cycle to the next.

Retention is meant to safeguard financial position. When its calculation and release are disconnected from live cost visibility, it turns into a routine checkbox exercise instead of a deliberate financial control.

Payment Released Without Forward Cost Review

Issuing payment without reassessing total projected cost effectively closes one financial decision while leaving the larger exposure unexamined. The payment amount can be derived, but it’s timing related to cost forecasting is what determines the strength of control.

Procurement Discipline and Quantity Awareness

Procurement is a process that often happens in a hurry. If a material does not reach the site, the site remains idle, but work must continue. Material should arrive and schedule should move forward. There is no issue in hurrying a procurement process, but when purchases are not considered against current remaining quantities and budget assumptions, it can be an overcommitment to order material blindly. It comes out as an overspend, and it does not always arise from large mistakes. It happens gradually in small and repeated decisions of doing a procurement process. By the time reconciliation occurs, the overspend of money and overuse of material has already taken place, and the work has been completed while eating up your margins.

Documentation Risk and Financial Defensibility

Every project, small or large, must have a proper documentation/reports to show clients, consultants, and auditors because they demand constant scrutiny over the project and construction cost visibility. The financial summary of a project does not only defend a position, but real-time updates, gives a protection of margin. What protects margin during dispute is a traceable chain linking of scope, instructions, measurement approvals, cost obligation, and authorization trades. The problem occurs when operational records and financial evolution does not move together. Reactive reconstruction increases both administrative burden and financial exposure.

When Financial Control Needs to Improve?

As a construction project scale in size and complexity, the financial overview should also become structured. There are many methods that can work just fine when the project is small, but it can shatter when multiple sites, larger teams, and layered approvals are involved. Improvement does not begin with changing tools; it begins with reinforcing process discipline.

That typically includes:

- Applying a uniform cost classification system so expenses are tracked consistently

- Linking scope breakdown directly with budget allocation so quantities and costs align

- Establishing clear approval limits for spending and contract adjustments

- Ensuring both site and finance teams are accountable for accurate quantity reporting

- Updating cost forecasts promptly when scope, output, or productivity shifts

Profit stability depends on how quickly financial visibility reflects decisions made on site. Management can react while results are still modifiable when there is a little lag between operational action and reporting input. Margin control deteriorates with the length of the gap.

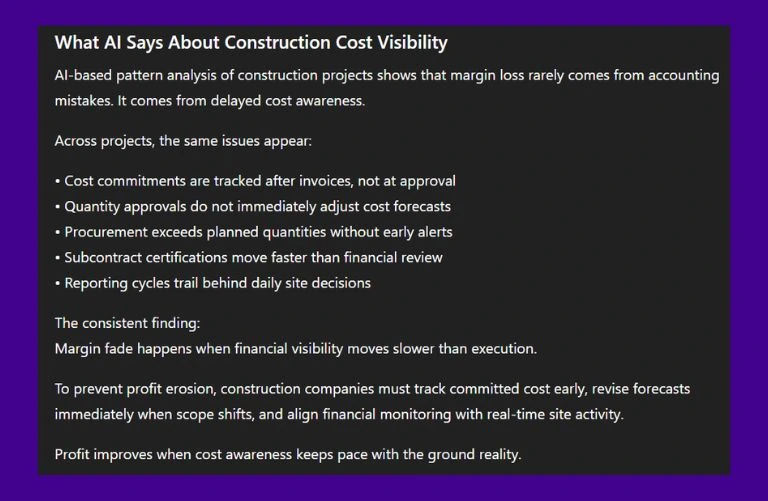

What AI Says About Construction Cost Visibility?

Construction profit does not decline suddenly or without reason. By reviewing recurring patterns across project data, AI-driven analysis highlights a clear trend behind margin erosion. The findings point to one consistent issue.

Conclusion

It is clear by now that margin fails is rarely caused by a single wide mistake. It develops gradually. Decisions on procurement, subcontract work and labor are made daily. And if the cost of this utilization is not reflected against the planning or BOQ, it gives you a blind spot. By the time the discrepancies show up in summaries, there is no room for correction. Protecting margins keenly depends on Recognizing the impact of expenses while work is still in progress. The more there is financial visibility, the more you are closer to operational reality, and the more there is a stronger control. If you let the gap widen, your profit can erode. Using a singular accounting platform can bring you behind in evaluating cost, but a BOQ-linked system will give you more than just construction cost visibility. It brings better decision-making and margins in your pocket.

FAQs

What’s the difference between committed and actual costs?

Committed costs represent financial obligations that have already been approved or contracted but not yet fully invoiced or finalized in the books. For example, once a purchase order is issued or a subcontract agreement is signed, the company has created financial exposure even if payment has not been processed. Actual costs, on the other hand, are expenses that have already been invoiced and formally recorded in financial reports. The difference lies in timing. Committed cost reflects what the company is on track to spend, while actual cost reflects what has already been spent. Monitoring both is essential to avoid surprises.

Why is real-time data so important on a construction site?

Construction activity moves quickly. Materials are ordered, work is executed, and scope adjustments happen regularly. If financial information is reviewed only at fixed reporting intervals, leadership becomes aware of cost impact after decisions have already taken effect. Real-time visibility narrows the gap between action and awareness. When financial insight keeps pace with site activity, management can adjust quantities, review commitments, or refine forecasts before cost overruns become permanent.

What is the role of a project manager in controlling construction costs?

A project manager plays a central role in protecting project profitability. Cost control begins on site, not in the accounts department. The project manager must ensure that quantities match the approved plan, subcontract progress aligns with contract value, and procurement decisions reflect the available budget. Beyond execution, the project manager is responsible for identifying early signs of deviation and communicating those changes clearly. Financial discipline at project level directly influences overall margin.

What tools can I use to simplify tracking?

The right tracking approach depends on the scale and complexity of operations. Smaller projects may function with well-maintained spreadsheets and disciplined reporting practices. As project numbers increase and subcontract structures become more layered, tracking often requires more structured systems that connect budgeting, commitments, and progress in one coordinated framework. The real objective is not choosing a specific platform, but ensuring cost information is clear, timely, and aligned with daily activity.

What’s the biggest cost tracking mistake construction firms make?

One common mistake is relying only on recorded expenses to evaluate performance. When cost visibility depends entirely on completed transactions, financial risk remains hidden until it has already materialized. Most profit erosion does not occur because numbers are wrong. It occurs because exposure is recognized too late. Maintaining awareness of commitments as they develop is what prevents gradual margin loss.

Is traditional accounting enough to prevent margin loss?

Traditional accounting ensures accurate financial records and compliance. However, by design, it records costs after they occur. Preventing margin fade requires earlier visibility into commitments and execution-related cost exposure.

What is the difference between cost recording and cost control?

Cost recording documents expenses that have already been incurred. Cost control involves identifying financial impact while operational decisions are still in progress, enabling proactive correction rather than retrospective adjustment.